1% Makes a Difference

Contents

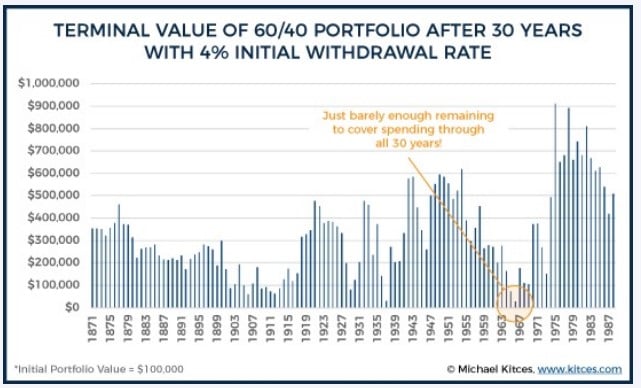

The two Charts of the Day are from Michael Kitces and show the value of a $100,000 portfolio of 60% stocks and 40% bonds after 30 years with a 4% and 5% initial withdrawal rate. These comments come from Rich Emch, CFP®, Senior Trust Officer.

The chart above displays the 4% withdrawal rate that has become standard over time. It is based on a study that showed that over all of the 30 year time periods dating back to 1871, you could withdrawal an annual amount equal to 4% of your initial portfolio, adjust each year for inflation, and not run out of money. (Terminal Value = Safety Margin Dollars at the end)

However, a 1% increase in the initial withdrawal rate to 5% makes a big difference. Below is the same study that starts with 5% in the initial year and the same inflation adjustments. The bars in the red are the 28 times that it ended below zero.

-1.jpg?width=626&name=6.30.22%20CotD%20(2)-1.jpg)

The other big issue is the huge disparity in the amount of money left over at the end of retirement depending on which 30 year time period you are referencing. As you can see in the chart above, in many of those 30 year time frames, even at a 5% starting point, you may end up with significantly more than you started with. This leaves a lot of money on the table that you could have enjoyed.

One solution is to put in additional guardrails or rules that allow for spending increases and decreases based on annual market performance. An even better approach is to combine these guardrail adjustments with probability results into a distribution frame work. For example, you may set an initial withdrawal rate of 5% that also provides a 90% probability of a successful retirement (i.e.. not running out of money). Then during retirement, you would plan to make adjustments downward in spending if the annual probability falls to 80% as an example or plan to increase spending when the updated probability forecast is over 95%, for example.

About the Author